Clinics in Malls – Insights from Raffles Medical

Come October 2021, malls have begun to reopen in India with full energy and they are preparing themselves for a successful festive season sale – to make some well-deserved money after dull and challenging 18-months of pandemic. While this is obviously a good tactical plan, my mind veered towards possibly some fundamental changes that they could adopt to de-risk their dependence on ‘shopping’ journeys alone. Can they look at other categories of ‘tenants’ which go beyond shopping only? I had covered some ‘Experience-based’ ideas in the very 1st edition of Outside In already last year – Saving Neverland -

In this edition, we look at the potential of leasing rental spaces for clinics (of various types) in malls. There’s no exclamation against this idea, because it is not a new idea at all. In fact, it is a very mature idea in the wider APAC region – barring India. For the purpose of this article, I will refer to some stories and examples from Singapore – where I have personally seen and visited these clinics – in Malls.

Let’s read up on what those Illustrations are and the possibility for malls in India, to explore this opportunity. Here goes…

Snippets from Singapore

General Practice

Dental Care

Holistic Healing

Pet Care

You get the drift right? These are all illustrations of clinics that are established within mall spaces in Singapore – and in my estimate – will literally create a new revenue stream going beyond shopping – under the activity of ‘daily healthcare formats’.

Advantages for Consumers

Assured parking spaces and cab ecosystem

Friendly and ample accessibility options – Wheelchair ramps, Elevators, Escalators

Clean environments

Access to utilities – Washrooms, ATMs, Food Court, Etc. (especially if there is waiting involved)

Feel-good vibe of a well-spaced-colorful-buzzing place (vs. drab outlets in crowded markets)

Advantages for Malls

Regular walk-ins which are not dependent on shopping

New category of tenants – whose nature of business is (by design) a longer lasting ‘service’

Steady rental/revenue-stream through the year

Some Traffic even on lean weekdays

Incremental shopping revenue (for stores and thereby the mall)

Advantages for Clinics

Premium ‘address’ – Move from unorganized space to organized space

Possibility of higher footfalls & regular patronage

Reasonable/planned rental roadmap

Access to superior (mall) infrastructure, ambience and common area services

Network opportunities – multiple clinic partnerships with same mall player across a city

Fair enough, this sounds interesting. So can we study this idea in some more detail?

Raffles Medical in Singapore Malls

Let’s use the experiences of Raffles Medical initiatives with multiple Singapore Malls – to study this.

A) Build out a Singapore-wide Footprint – Mix of Exclusive Hospitals/Clinics & Mall-located Clinics

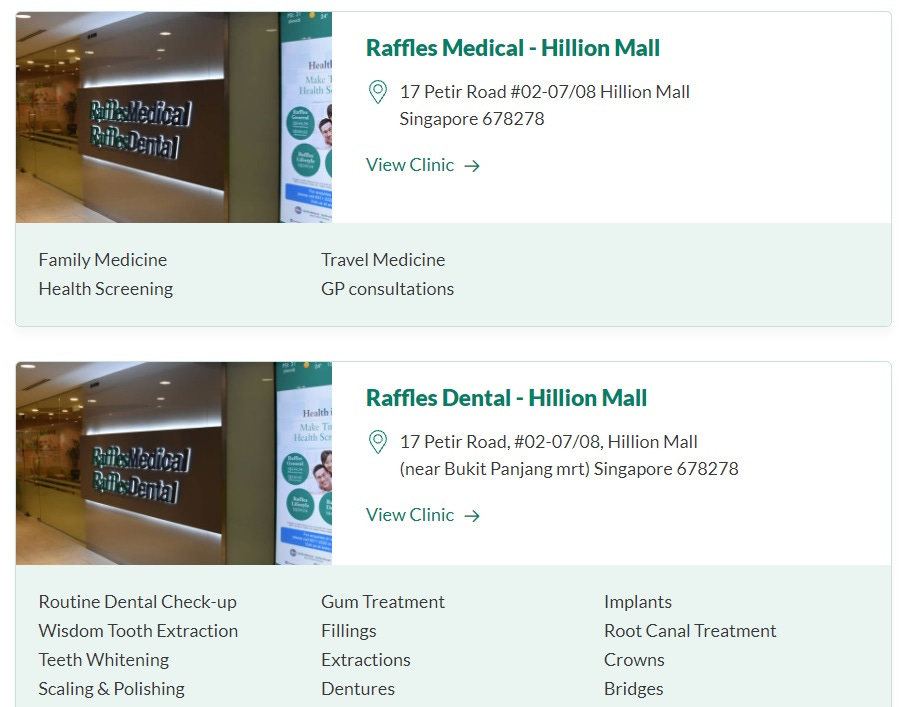

B1) Service Offerings – Raffles Medical and Dental at Hillion Mall:

B2) Services Offerings – Raffles Medical at Eastpoint Mall:

Raffles Medical ‘Retail/Mall’ Approach – A Hub & Spoke Model

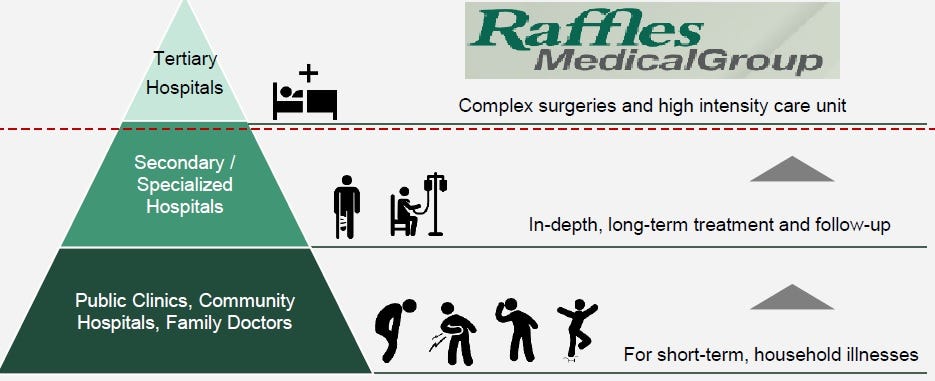

RMG operates through 3 different segments: hospital services, healthcare services and investment holdings. The hospital services segment is engaged in the provision of specialized medical services and operation of hospitals. The segment also engages in the business of medical laboratories and imaging centers. The healthcare services segment is engaged in the operation of medical clinics and other general medical services such as health insurance, trading of medical equipment and the provision of management and consultancy services. In the healthcare services segment, they operate primary medical care, dental and traditional Chinese Medicine clinics located all around Singapore. This segment serves both – private as well as corporate – segments. The rationale behind the adoption of this model for RMG is: 1) to reap economies of scale through shared resources and enhanced presence and, 2) to have a totally integrated platform operating across the whole value chain

RMG operates across the entire healthcare spectrum (primary, secondary and tertiary). One way it drives patient growth is by feeding patients from its clinics to its hospital. This creates customer stickiness by making it more difficult for patients to admit themselves into other hospitals. It currently has more than 6,500 corporate clients –notable ones include DBS, Singapore Airlines and Google. This provides RMG with a source of steady and recurring revenue due to a strong reputation for corporate healthcare and positioning as a leader in providing healthcare screening services

In Conclusion

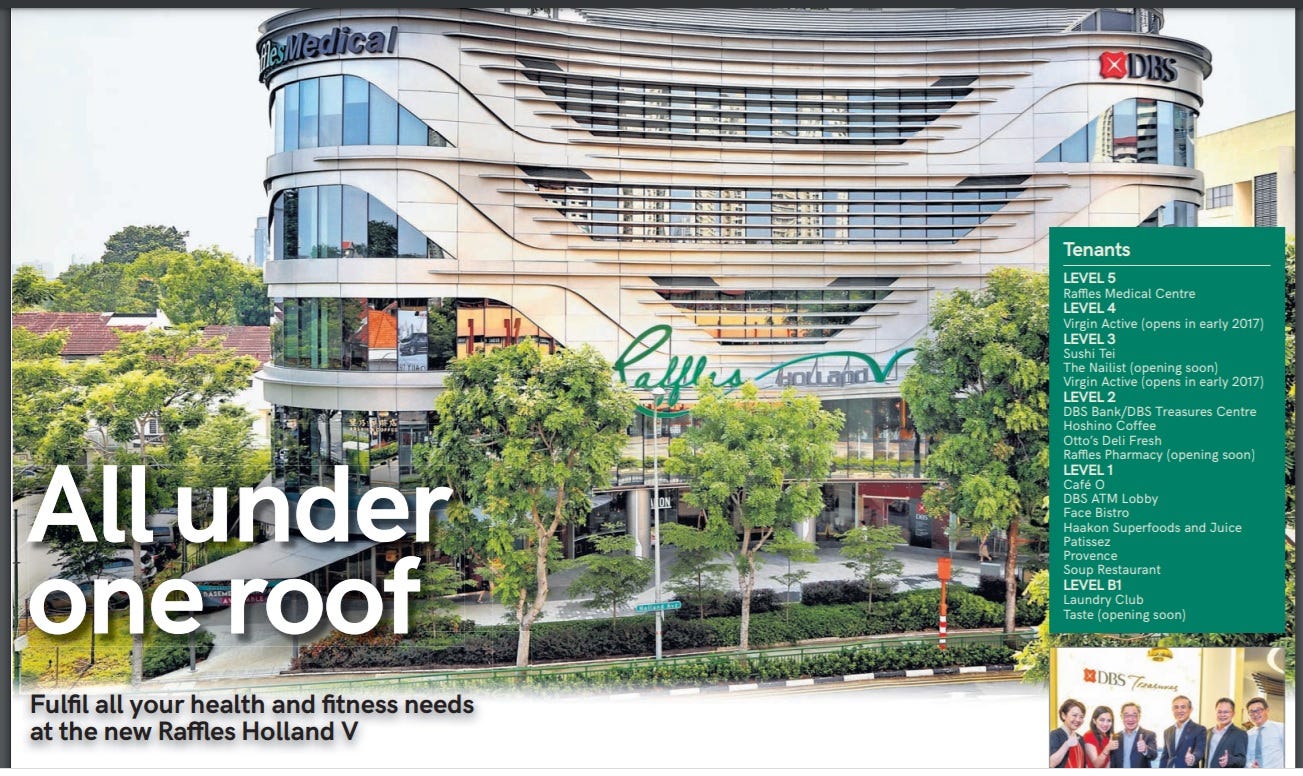

In fact, I think the model is working so well for Raffles Medical that, in 2016, they moved up the ‘mall value chain (if we can say)’ by opening a new mall on their own – which will blend Medical and Retail by design

Here’s the outcome of that Initiative – Raffles Holland V

Will the likes of Fortis, Apollo, Manipal and Reliance HN Hospitals visualize such a play? And, set up ‘mall-avatars’ of their Services for future Growth? I think they should be definitely exploring… Maybe, a leading mall player can invite them proactively!

References and Sources:

1. Raffles Medical Own Mall: https://www.rafflesmedicalgroup.com/wp-content/uploads/2020/07/raffles-medical-39-s-new-mall-to-open-soon.pdf

2. Raffles Holland Centre: https://www.rafflesmedicalgroup.com/wp-content/uploads/2020/07/all-under-one-roof-raffles-holland-v.pdf

3. CFA Report: https://www.cfainstitute.org/-/media/regional/arx/post-pdf/2020/02/20/singapore-singapore-management-university.ashx

4. Raffles Medical Website: https://www.rafflesmedicalgroup.com/our-group/about-us/our-heritage/